Scaling your Business with Revenue Planning

Revenue planning is essential for ensuring the longevity of your company. It doesn’t matter if you’ve been an entrepreneur for a few months or several years. A business will grow for years to come if you have a solid revenue strategy in place.

Companies have recently discovered the importance of cross-functional alignment, which aids in creating a better growth strategy and promotes consistent customer experiences.

Let’s examine the revenue planning process and discuss why you should do it for marketing and sales planning.

What is revenue planning?

Revenue planning assesses how a company will make money and what to do with it. In other words, would you use the money from sales to spend on costs? Or to make investments, like hiring more people or buying more things to sell?

When you know how much your project will earn, you can calculate your company’s revenue from other sources. This will help identify the kind of worthwhile investments.

According to financial solutions expert Jeff Sobers, an efficient and effective billing process generates revenue, lowers the cost of doing business, and boosts cashflow – all of which are essential to a healthy, thriving, and long-lasting business.

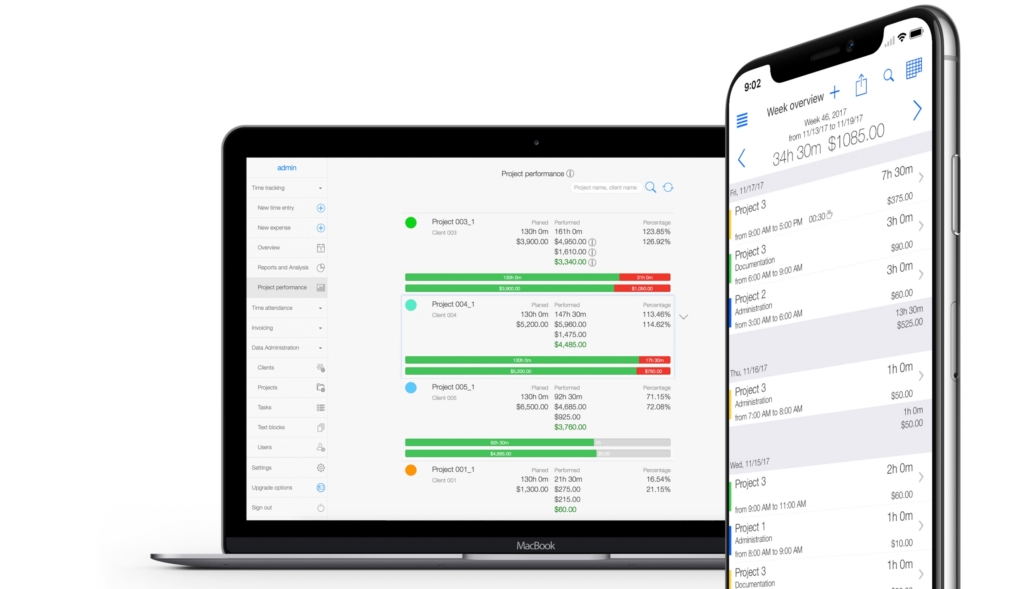

TimeTrack’s Project Invoicing feature comes in handy here. The process is simplified with automated project time tracking to form the basis of project invoicing. An efficient invoicing system is crucial to revenue planning for any business, whether big or small.

TimeTrack Project Invoicing

Why revenue planning is important

When a company performs revenue planning, it can estimate how much cash it will receive from various sources. Predictions regarding future income and how that revenue will be utilized are essential for any organization.

By figuring out how much the business will make, CEOs can plan for business growth and future opportunities. Revenue planning also gives much-needed insight into how to structure employee salaries and how much is needed to acquire company resources.

This information gives managers perspective on how long the company can stay afloat if sales falter, if there’s a downturn on the market and if the business is on track to meet its revenue projections by monitoring its revenue forecasts and costs. They can then use this data to change their strategy and set updated realistic goals.

Revenue planning process for small companies

Without a good cashflow estimate, a business can’t plan its income well. The first step of revenue planning is to know how much money is expected to be generated and spent over the next 12 months.

Estimating a company’s income for the next year unlocks important information about how to spend money. (That is, to pay for business expenses in the future.)

Say a business wants to hire a new employee. Revenue forecasting can help determine how much that salary will account for and if the money coming in from sales will be enough to pay for it. Besides hiring staff, you will need to consider how different things might affect your income forecast.

Revenue planning determines how much money a business will produce when it comes in and if it will have enough cash to continue. Here are the most important factors when doing revenue planning once you have gathered all the data.

-

Focus on a clear timeframe

Focus on last year’s (or another past period’s) revenue goals and see if they were met to start the revenue planning process. We recommend using a fiscal year because it helps keep things organized, but if a small business is new, forecasters can also look at the last six months or the last quarter. Assess the sales planning goals and determine if they were met, exceeded, or fell short, and by how much.

-

Get clear on your goals

Start with the goals, as you would with any plan. The most important question is: What does a business want to do and why?

But be sure to split that question up into a few different ones:

- How much money would you like to make in the next year? Next three years? How many employees would the business want to hire in the next year? Coming three years? Five years?

- Details are important. A “Well, let’s see how it goes” attitude won’t motivate you or the employees and just creates confusion around goals and objectives.

- It’s easy to get off track when trying to finish everything on time. A time management checklist can help you keep your mind on the task at hand and avoid getting sidetracked. Use it to set realistic targets for the sales team to make sure they don’t waste time on minor things.

3. Assess where the company currently stands

To determine how much a business can grow, look closely at its current assets, liabilities, people and systems. This data helps businesses avoid the risk of developing an unsustainable expansion strategy.

Businesses often overestimate what they can do in a short time and underestimate what they can do in the long term.

Things to keep in mind

-

Make operating budgets for marketing & sales efforts

Use the current growth budget and how much the business made from different marketing and sales efforts to estimate how much more it will make. For example, Marketing spent $3, 000 on Facebook ads, which led to sales of $10,000. That means that if they spent $6,000, it could double their income.

Even so, there is a good chance that not all predicted outcomes will pan out. But seeing how different predictions play out gives you a better idea of what could happen. And it also helps you make better business decisions for long-term success and course-correct when necessary.

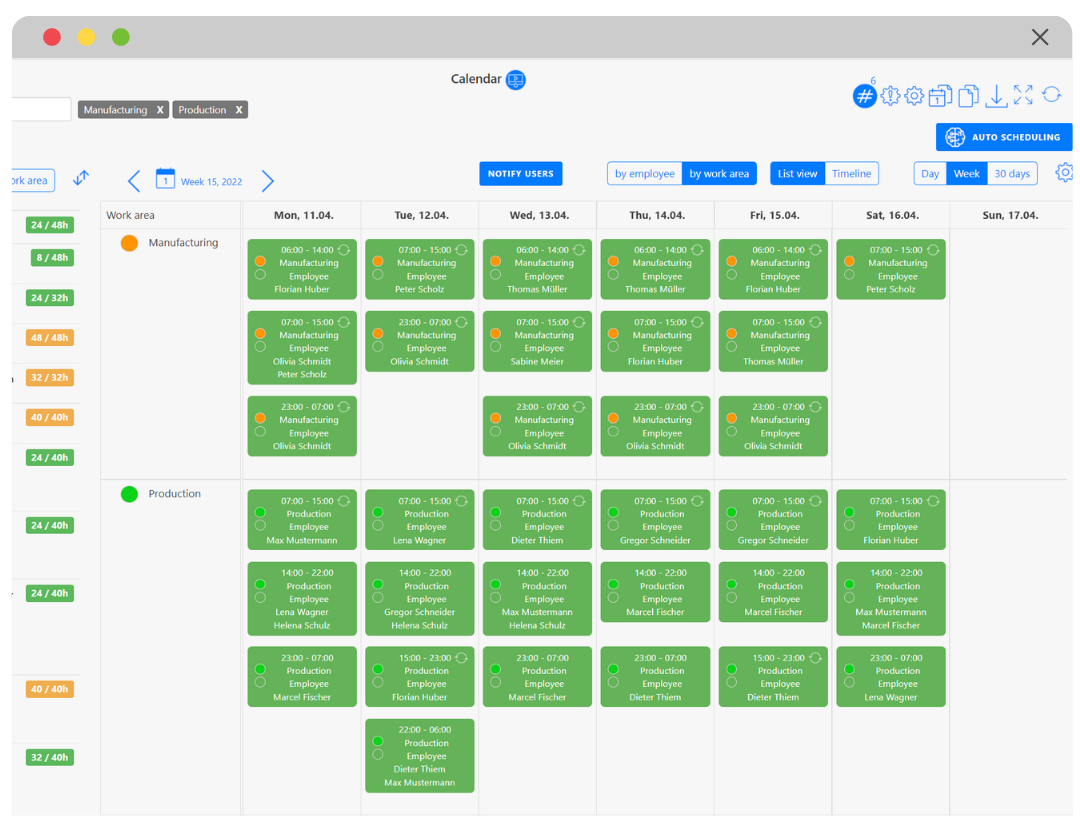

To create synergy between various departments for revenue growth, use TimeTrack’s automatic scheduling feature. It creates a simple and clear duty roster with just one click, in which employees know exactly when and what to work on.

TimeTrack Auto Scheduler

Budget forward for revenue growth

Establish a budget and evaluate your progress in light of the growth objectives. For example, if the revenue stays the same for the sales team, how much does the business have left over after paying all the costs, including salaries? Put this information to use for reliable revenue forecasting and future profitability.

Tips for planning international revenue streams

Many businesses find going global exciting; for others, it is a pressing and sometimes stressful reality. New markets. New customers. New ways to make money. High rates of return on cash invested. Revitalized product development. There’s so much to consider.

“Internationalization” is a strategic move that many organizations use to start the next chapter of their growth process on a global scale.

1. Remember to audit

An internal data audit lays the groundwork for a smooth, successful expansion. It’s a symbolic roadmap covering every data point, turn, stop and speed bump before a brand goes international.

An internal business audit should be thorough and focused on details. Stakeholders from all parts of the organization, such as operations, sales, marketing, finance and IT, should be involved. These areas will need to grow and work together for the overseas rollout to do well.

Each department’s ideas and infrastructure need to be looked at, tested to see if they will work, and then changed to fit the new market for revenue planning.

-

Strike it while it’s hot

As the saying goes, your reputation precedes you. It is easiest for a business to grow internationally when its domestic market share, capabilities, operations and brand perceptions are stable and strong.

New initiatives and efforts are built on a solid domestic foundation. Overseas markets will still have access to the impressions of the core market, PR and marketing campaigns and how customers think a company does business.

Everywhere a company goes, it takes its reputation with it. Make sure that it is a good one.

A business maturity model can be used to assess an organization’s effectiveness and constantly improve business operations. These demonstrate the degrees and commercial goals for key phases and disciplines of management. A business maturity model gives feedback and recommendations to firms to enhance their maturity, capabilities, operations and procedures.

-

Don’t rush it

To be a “first-mover” means to be a company that introduces a revolutionary new product or service to a market. This form of growth can be a never-before-seen commodity that is truly unique and has no evident competition. Or it can be disruptive, changing how people see or use a service that has already been around for a while.

Plans to be the first internationally are often very aggressive. This is because being the first means establishing and dominating international market shares, leaving those who come later to pick up the scraps.

But innovation isn’t based on a set of rules, which is both good and bad. The best strategies for expanding overseas are flexible and well-thought-out. They require diligence, nuance, commitment, detailed resource planning and buy-in from executives and stakeholders from different departments.

-

Match the business model with mode of entry

Business models include how an organization runs, interacts with others, makes money and creates products or services that add value. In short, these models show how a business works.

But not all models are the same. Processes in one country may not always work well in another. Also, there will be new organizational hierarchies, new resources for products or services to find and new employees to hire and sort, each with their own culture and expectations.

All this means that a plan to expand internationally must include a business model that has been tweaked to do two things at once:

- Matches the expected value of a foreign market (i.e., why you chose to expand there). These reasons could include making products more cost-effectively, getting more customers, extending a product’s life or taking advantage of tax breaks in the new market, to name a few.

- In sync with the genuine culture and customs of that emerging international market.

Benefits of revenue planning

To achieve long-term success and sales performance, businesses must coordinate their marketing and sales teams with revenue forecasting efforts. With this understanding, top management must continue to set precise targets and then delegate responsibility for meeting those targets to individual department heads.

Even in the best of teams, members working independently to achieve common goals can provide varying outcomes and inconsistencies in revenue planning, resulting in subpar output.

Customers’ preferences and industry trends constantly change, so businesses need up-to-date technology, training and knowledge. An efficient planning process helps companies determine what they need and how to meet those needs. It also helps businesses use the people they already have and put them to better use.

With a good planning process, CEOs can find the holes and risks that could slow or stifle growth. Strategic growth is driven by taking calculated risks.

Be confident in the risks and back them up with data, a sound plan, a thorough understanding of the market and input from your dynamic and diverse team of experts. A well-thought-out strategy is essential but the true engine that stimulates growth trajectory is ambition and drive.

Conclusion

As a new or established business, revenue planning is a vital cog in your company’s engine. Take the time to research market and industry trends, emerging data and established processes to create the most applicable strategy for your company.

It’s possible that one might not have the time or money to devote to producing reliable financial statements or making thorough financial projections for revenue planning through an accounting system. Schedule a free demo with TimeTrack if you want real-time data about your company’s health and require assistance gaining access to reliable revenue forecasting.

Anja Bosiok ist Marketing Managerin bei TimeTrack und schreibt seit über drei Jahren über Zeitmanagement, moderne Arbeitswelt und digitale HR-Prozesse. Sie studierte Journalismus (Bachelor) sowie Publizistik- und Kommunikationswissenschaft (Magister) und verbindet redaktionelle Präzision mit tiefem Produktverständnis. Zuvor war sie als Content Managerin bei TimeTrack tätig und begleitet seitdem die Themen rund um Arbeitszeiterfassung und Personalorganisation – von der gesetzlichen Grundlage bis zur praktischen Umsetzung im Unternehmensalltag.